AST SpaceMobile Skyward Bound

AST SpaceMobile is on a path to a $50-100 billion market cap.

Last year, I penned an article highlighting AST SpaceMobile's (NASDAQ: ASTS) leadership in the race to deliver cell phone service directly from space to mobile devices. The piece, titled AST SpaceMobile Screams 'Watson, I'm Calling You From Space, captured the company's innovative edge.

Since then, AST SpaceMobile's stock has soared by over 250%. During this period, subscribers to my service have been strategically accumulating ASTS shares and selling cash-secured puts to generate income.

The common temptation with a rapidly appreciating stock like AST SpaceMobile is to sell or trim positions, driven by the often misguided notion that "nobody ever lost money taking a profit."

However, I am committed to riding the wave with AST SpaceMobile, as I believe its potential extends much higher. I continue to rate AST SpaceMobile shares as a strong buy, just as I did last year.

I encourage you to explore AST SpaceMobile's website and review their Investor Presentation and SEC documents for essential background information. My focus is on delivering analysis that I believe the market is overlooking rather than regurgitating widely available information.

A Chat With AST SpaceMobile President Scott Wisniewski

Last month, I was able to spend a half-an-hour on a call with AST SpaceMobile's Chief Strategy Officer Steve Wisniewski. A day after our talk, he was made President of AST SpaceMobile. It was a great conversation.

I asked several key questions, and I got clarity on whether some of my bullish analysis was more or less likely to prove true over time. Here's the short version paraphrase of what we talked about:

Me: Will the 5 satellites (for North American cell coverage) planned to launch in September be delayed due to the SpaceX rocket issue last month?

Scott: To the extent they have to delay things, we could see a delay too. If your flight is delayed, you don't go next. They don't shift the entire line. You go to an empty time slot in the future. So, could be a little later than anticipated before the recent rocket problem. It appears the problem is fixable (indeed, SpaceX just resumed doing launches again).

Me: I have been trying to model revenues and free cash flow out over the next 5 years or so to when all the satellites are up. I keep coming up with big numbers in the billions for annual revenues and free cash flows. China is probably out as a customer and India is hard to always penetrate from what I've read and seen. How should I be thinking about customers and revenues?

Scott: We haven't issued any forward guidance on that. But, I think in markets like the U.S. you will see monthly subscription fees in the $10-15 range, and we get half of that, the MNO (Mobile Network Operator) the other half, so pretty straight forward. It's an incentive for the MNOs, who are growth challenged, to increase revenues by offering the service. AST SpaceMobile margins should be very high given periods where we have very low capex.

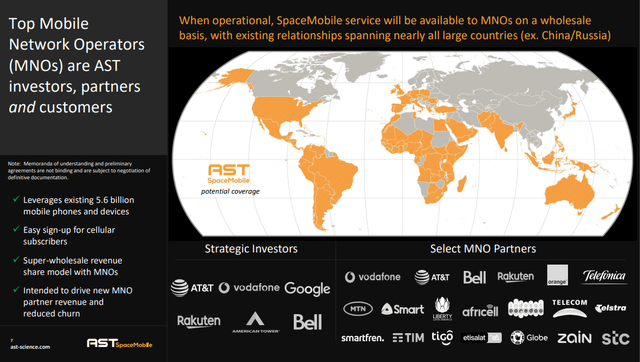

We have the two biggest cell providers in the U.S. in AT&T (T) and Verizon (VZ). As we go global with the next batch of satellites, there are over 2 billion potential customers. Vodafone is a big partner. So is Rakuten and Telefónica. We're up to about 50 MNOs, I think the last time we mentioned it, we were at 45. China are not going to use us it wouldn't seem. Vodafone does have a presence in India (about 200 million accounts). South America we have good coverage. Africa is growing and we have agreements there too.

Me: How often do the satellites have to be replaced and does a shift to 6G in the next decade make a difference?

Scott: In low earth orbit, satellites need to be replaced about every 7-10 years. So, there will be periodic capex, but spread out over windows using cash flow. The maintenance is fairly low during those multiyear windows when capex is very low. An upgrade to 6G does not impact us as our satellites are G agnostic. The conversion to use the spectrum happens at the MNO so we are "G agnostic."

We discussed a few other things that really had to do with clarifying my understanding of the technology from their patents which are heavily protected and how Nokia (NOK) radio technology makes a direct to cell phone signal more reliable.

Ultimately, I came away with the idea that the company is now transitioning from the science-based building of the company to taking the product to market and making the most of their first mover advantage.

1st Mover Advantage

AST SpaceMobile is poised to capitalize on a significant first-mover advantage in the realm of direct-to-cell 5G service, as no other company is currently close to delivering this capability. With an estimated lead of three to five years, AST SpaceMobile is strategically positioned to dominate the market. Their aggressive pricing strategy is designed to capture a substantial market share quickly.

In a recent investor note, Scotiabank expressed a bullish outlook, stating, "We believe ASTS has the potential to become the world’s largest wireless company by subscribers."

I concur with this assessment. The sheer number of potential customers is unparalleled, thanks to AST SpaceMobile's contracts with approximately 50 Mobile Network Operators (MNOs). While competition will eventually arise, AST SpaceMobile could already have over a billion full-time (subscribing monthly) and part-time (using services while traveling) customers by then.

Currently, AST SpaceMobile has agreements that could potentially cover around 3 billion people. This includes both relatively affluent nations where 5G is anticipated and emerging markets that currently lack 4G/5G access. With additional MNO deals, coverage could eventually extend to nearly 6 billion people.

The pricing model is compelling: a $10 monthly fee as an add-on in wealthier nations (about 2 billion people) and as a full-service broadband offering in regions without existing tower networks (approximately 3.7 billion people). I anticipate triple-digit growth rates until a year or two after the full constellation deployment. Although the law of small numbers applies, each of the three major deployments planned over the next few years will introduce a significant number of new potential customers.

The likelihood of surpassing a billion customers is substantial, and I would estimate better than a coin flip chance that they reach this milestone by the end of the decade. Given the current and potential future MNO deals, aiming for 2 billion full and part-time customers is a realistic goal for AST SpaceMobile.

Back Of The Napkin Math For AST SpaceMobile

With the upcoming launch covering the United States, AST SpaceMobile is poised to tap into a significant market. AT&T and Verizon, two major U.S. carriers, have a combined customer base of approximately 230 million. According to Pew Research, about three-quarters of Americans are at least casual travelers. This translates to roughly 170 million potential U.S. customers who might be interested in AST SpaceMobile's service, as those who do not travel likely do not prioritize connectivity outside their residential areas. To be conservative, let's focus on this subset of potential customers.

It is estimated that 10-20% of these potential customers, likely those in the "investor class," would be willing to pay $10-15 per month for connectivity when beyond cell tower range. Using the lower end of this range, approximately 17 million full-time customers could be expected.

At the minimum price point of $10 per month, and with AST SpaceMobile retaining half of the revenue (as per their agreements), this translates to $85 million per month or over $1 billion annually in revenue. With expected margins of at least 50%—and potentially much higher—this could result in over $500 million in free cash flow annually.

Moreover, it's anticipated that most Americans will use AST SpaceMobile's services intermittently during travel. As Pew indicates, the average American travels two to three times per year. Assuming they use the service once during these trips, this adds approximately 136 million paid months, generating another $1.36 billion in annual revenue and around $700 million in free cash flow.

A conservative estimate of AST SpaceMobile's free cash flow from the U.S. market alone is around $1.2 billion per year. These figures are considered fair to light, providing a solid foundation for the company's financial projections.

Looking ahead, AST SpaceMobile plans to expand its coverage to additional Mobile Network Operators (MNOs) worldwide. If the company secures 100 million full-time subscribers globally, this could generate $12 billion in annual revenues. Additionally, if a billion people use the service on average for one month per year, this could add another $10 billion in annual revenues.

If AST SpaceMobile's projections hold true, with revenues exceeding $2 billion per month and a conservative margin of 50%, the company could achieve free cash flows of $1 billion per month, or $12 billion annually. This financial performance could significantly impact AST SpaceMobile's valuation.In the private equity space, businesses are typically valued at about six times their free cash flow, depending on the industry. Applying this multiple, AST SpaceMobile could potentially reach a market cap of $72 billion by the end of the decade. For comparison, American Tower (AMT), an investor in AST SpaceMobile, currently has a market cap of about $99 billion with unlevered free cash flow of $5.6 billion last year.

While these projections are based on back-of-the-napkin calculations, they illustrate the rapid revenue growth potential for AST SpaceMobile. As the company continues to expand its satellite network and secure strategic partnerships, it is well-positioned to become a significant player in the global wireless market. The future financial performance will depend on various factors, including successful satellite deployments, market adoption, and competitive dynamics. However, the potential for substantial growth and market impact is evident.

Investment Thoughts On AST SpaceMobile

My clients made AST SpaceMobile shares a full position in their portfolios between last April and this spring with a scaling in approach. We consider a full position to be 3-4% of portfolio value. I have also sold puts along the way, further defraying my net cost for the position.

I still see ASTS shares as a "buy the dips" stock and for many of us, it will be a "sell cash-secured puts on weekly oversold conditions" stock.

Kevin Mack, a lecturer and researcher at Stanford's Graduate Business School, noted that it appears there has been institutional buying in ASTS shares recently.

When institutions increase their holdings, it often exerts upward pressure on the stock price, especially since insiders hold about 75% of the shares, net of dilution, according to Fintel.

I view any volatility caused by such forced selling as an opportunity to buy ASTS shares at a lower price. For those familiar with the strategy, selling cash-secured puts can also be advantageous if you are optimistic about the stock and volatility is high.

Personally, I have little intention of selling my shares until AST SpaceMobile fully capitalizes on its global market potential. I see this as a generational investment opportunity, with the potential 10-30 bagger from current prices.